Are you missing out on retirement savings?

Planning for the future can bring financial confidence. Here are some reasons why retirement contributions are so important and how you can get started.

Planning for the future can bring financial confidence. Here are some reasons why retirement contributions are so important and how you can get started.

Save Now for More Money Later

The sooner you start saving, the better off you can be in retirement. And who doesn’t want a solid financial future?

Let’s say you decide to start saving for retirement and save $200 a month until you retire at the age of 67. The table below shows how the balance of your retirement savings could change depending on how soon you start saving.

That’s if you consistently set aside $200—no interest, no investment dividends, just $200 a month. If you make those monthly contributions to an investment account with annual returns or compound interest, your balance could increase even more! Bottom line? The earlier you start, the larger your nest egg could be.

Ask your benefits manager about the retirement savings plan offered through your employer, like a 401(k), 403(b), or TSP. You can also consider opening an account on your own – common ones being a Traditional or Roth IRA (Individual Retirement Account). Visit the IRS website for qualifications and tax implications: irs.gov/retirement-plans/traditional-and-roth-iras. Most plans have an option for automatic deposits, so you don’t have to worry about remembering to contribute each month. Check the IRS website for current-year contribution limits: irs.gov/retirement-plans/cola-increases-for-dollar-limitations-on-benefits-and-contributions.

Keep in mind that each retirement account option has pros and cons, so talk with a Money Coach before moving forward. You can work with a whole team of Money Coaches, including retirement specialists, tax specialists, and more, so you can make a well-informed decision and choose the best plan for you.

Create a Strategic Plan to Achieve Your Retirement Vision

Imagine the confidence you could gain by knowing that your dream for retirement is possible. At MSA, we recommend the following steps to build your future.

- Create your retirement plan. This includes setting a target date for retirement, defining your lifestyle and vision, and determining how much to save.

- Stay on track to achieve your retirement goals by budgeting and adjusting as needed.

- Explore ways to increase your savings. Work to save at least 15% of your income towards retirement, even if you start slow and build up.

- Get started as soon as possible!

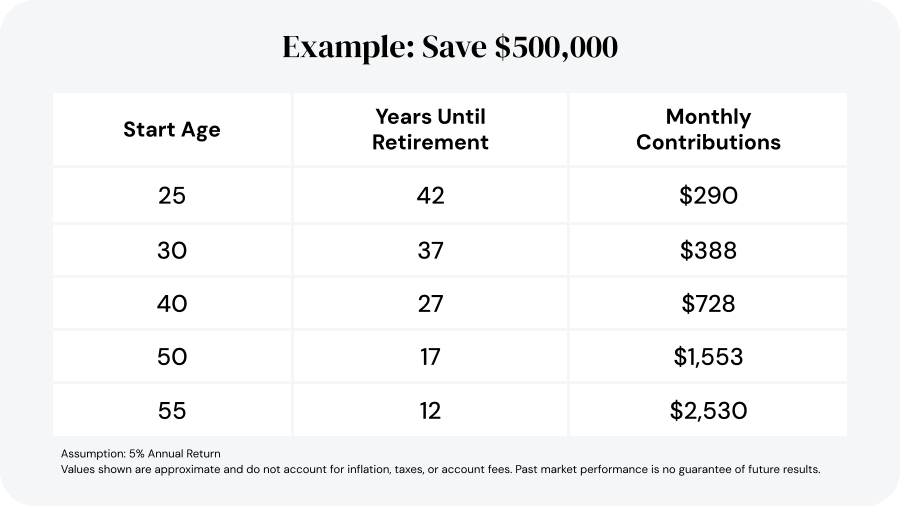

Here’s an example: say you have a goal of saving $500,000 by the time you retire at age 67. Here’s how much you would have to save each month in order to meet your goal, depending on how old you are when you start saving:

Would you rather save $290 a month or have to save $2,530 a month?

Not sure where to start? A good first step is to look at your monthly income and expenses. Once necessities are taken care of (e.g. rent, utilities, etc.), consider how much money you can prioritize and fund towards retirement.

Your Money Coach can direct you to calculators that can help you calculate how much you need to save for retirement and how much your contributions could amount to in the future. Your coach can also help you work on a budget that accounts for both long-term goals and daily expenses.

Are you leaving money on the table?

If you have an employer who matches your retirement contributions (meaning they also make contributions to your account based on certain parameters), but you aren’t contributing enough to get the match, you’re leaving money on the table.

Some employers match up to a certain percentage; for instance, an employer might match an employee’s contributions dollar-for-dollar for the first 3% of the employee’s wages and match fifty cents on the dollar for the next 2%. Here’s an example using those parameters: an employee who annually contributes 5% of their $50,000 salary would be putting $2,500 into their 401(k) each year with an employer match of $2,000. If that same employee only contributes 1%, he would be allocating $500 a year with an employer match of $500, which would mean that each year he’s leaving $1,500 on the table.

Ask your benefits manager if your employer offers matching contributions. If they do, consider budgeting to allow you to increase your contributions to get the full match. Keep in mind, though, that increasing your contributions could impact your take-home pay, so keep a close eye on your spending after you increase your contributions and make necessary adjustments to be sure you’re still living within your means.

Next Steps

Talk with a Money Coach who is a Retirement Specialist. Together, you can discuss retirement goals, create and implement an action plan, and gain confidence that you can live the retirement lifestyle you envision.

In addition, Money Coaches can discuss virtually any financial topic, so if you’re wondering about controlling spending, leveraging credit, preparing for the unexpected, or creating a game plan for your goals, reach out to a Money Coach. Call 888-724-2326 today.

___

The graphs/charts/diagrams are for educational purposes only. Your individual results may vary from those described.

See IRS Publication 590 for more detailed information about your IRA options.

Employer matching contributions may be subject to a vesting schedule that can reduce or eliminate employee access to employer contributions if they leave the employer within a certain timeframe. See your Plan Document or speak with your Plan Administrator to understand your employer matching contributions.

More Like This

Check out the resources available to you through My Secure Advantage (MSA)! This blog post provides resources specific to natural disasters and the recent California fires. My Secure Advantage Can Help Leverage the experience and peace of mind that a Money Coach can offer during this stressful time: Knowing where to start and how you […]

You asked. We listened. MSA Wallet® now offers a new suite of features making it easier to budget, save, and get a clear view of your finances. Our video takes you on a ride through MSA Wallet, and the details on the latest features are below. Check them out! More Categories Here’s the scoop: […]

Life is constantly evolving, and financial stability can feel just out of reach. Whether you’re adjusting to new routines, managing rising costs, or just trying to make ends meet, this is the perfect time to reassess your financial picture and explore some money-saving strategies. At MSA, we’re here to help you craft your own financial […]

We all know it’s easy to make a list, but completing the list is a whole other ball game. You can write “spend less” or “get out of debt” for your resolutions, but will you actually succeed? We’re here to say, “Yes!” This year, you don’t have to worry about watching the months go by […]